-1.jpg?height=100&name=Image%20from%20iOS%20(2)-1.jpg)

Winnie

Education Savings Accounts (ESAs) are state-run programs that give parents access to public K–12 education funds to spend on approved educational expenses. In other words, instead of all education funding going directly to a public school, a portion of those taxpayer-funded dollars is deposited into an account for the family to use for their child’s education. Parents can then use ESA funds for a variety of learning costs – from private school tuition and textbooks to tutoring, online courses, and specialized therapies.

Each state with an ESA program sets its own rules for who is eligible and what expenses are allowed, so the exact usage of funds depends on state-specific regulations. Generally, ESA funds are restricted to education-related costs only and distributed via debit card or reimbursements, with safeguards in place to prevent misuse. ESAs have expanded in recent years as a K–12 funding option in several states and are a key part of the broader school choice movement.

ESA vs. Coverdell Education Savings Accounts (CESA)

It’s important not to confuse state-funded ESA programs with Coverdell Education Savings Accounts (CESAs), even though both use the term “Education Savings Account.” A Coverdell ESA is a private savings account that parents can open at a financial institution to save for their child’s education, whereas a state-run ESA is funded by public education dollars. The table below highlights the key differences:

In summary: Coverdell ESAs are savings plans that parents fund themselves, whereas state ESAs are scholarship-like accounts funded by public money. To open a Coverdell or any similar account, you need to put in your own money (anyone can open one if they have the funds). By contrast, a K–12 ESA program provides funds to you if you meet the state’s eligibility requirements.

Coverdell ESAs also have some limitations (like a low annual contribution cap and income eligibility restrictions for contributors) that don’t apply to publicly funded ESAs. Coverdell accounts are available to everyone nationwide, whereas ESAs are only an option in certain states and often for specific groups of students.

ESA vs. 529 College Savings Plans

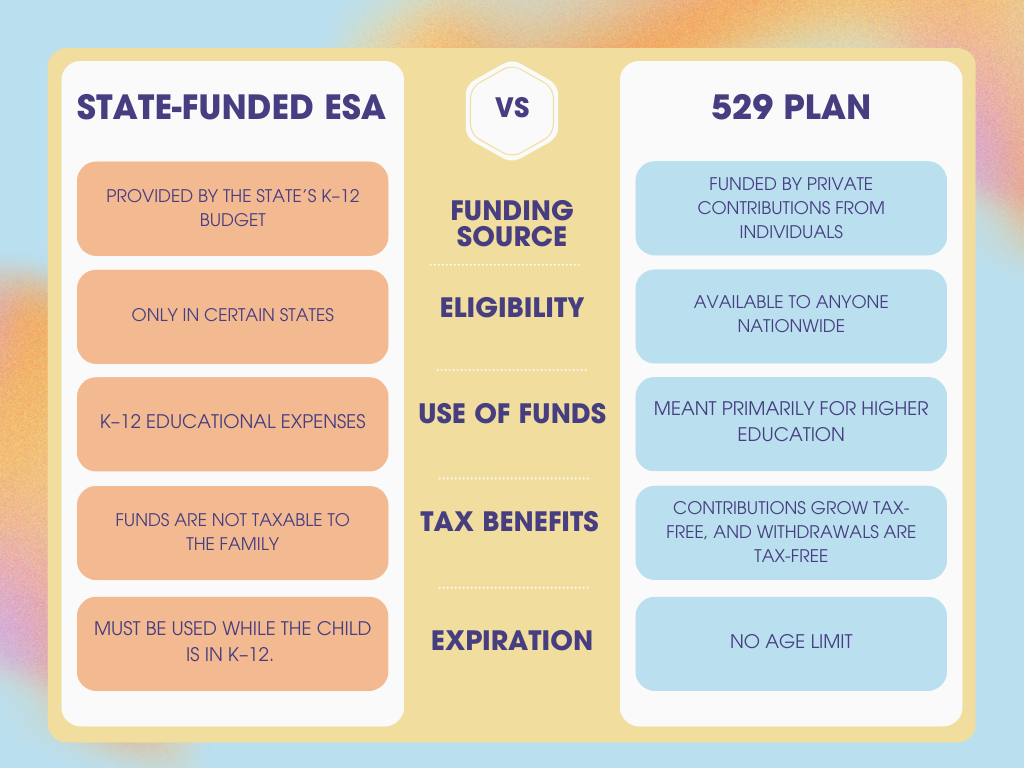

Another common source of confusion is the difference between an Education Savings Account (ESA) and a 529 college savings plan. A 529 plan is a tax-advantaged investment account designed primarily to help families save for college (higher education), although it can now be used for some K–12 expenses as well. Unlike ESAs, 529 plans are not funded by the state – they are funded by individuals (parents, grandparents, etc.) who contribute their own money. Here are the key differences between state-funded ESAs and 529 plans:

What is the difference between an Education Savings Account and a 529 plan?

The biggest difference is that an ESA (Education Savings Account) in the K–12 context is money from the government for current educational expenses, whereas a 529 plan is money you save for future education. If you have access to an ESA, the state is essentially giving you a portion of your child’s K–12 funding to spend on approved schooling costs now. In contrast, with a 529 plan, you are setting aside your own money over time to pay for your child’s education later (usually for college, although 529s can also help with limited K–12 tuition costs). ESAs depend on state legislation and are not available everywhere, while 529 plans are available to anyone and come with federal (and sometimes state) tax benefits.

ESAs and TK, Pre-K, and Junior Kindergarten

One common question for parents is whether ESA funds can be used for preschool or transitional kindergarten programs. In most cases, the answer is no – Education Savings Accounts generally cover Kindergarten through 12th grade expenses, not preschool. ESA programs are funded by state K–12 education budgets, so the benefits typically begin when a child enters kindergarten (or elementary school age as defined by the state). That means you usually cannot use a K–12 ESA to pay for Pre-K, TK (Transitional Kindergarten), or Junior Kindergarten programs at private or independent schools.

For example, if you have a four-year-old attending a private preschool, you would not be able to use an ESA (even if your state has one) to cover that preschool’s tuition, because the child isn’t yet in the K–12 range that the program funds. The ESA would become available once your child reaches kindergarten (assuming you meet any other eligibility requirements of your state’s ESA program). Exception: Some states might offer ESA-like accounts or scholarships specifically for students with disabilities that could start earlier, but generally standard ESA programs are K–12 only. Always check your state’s rules if you think there might be an early childhood provision.

What can parents do to fund early education? If you’re looking for help with Pre-K costs or want to find free preschool options, there are other resources and programs outside of ESAs:

-

Universal Pre-K: Many states now offer free, state-funded preschool programs for four-year-olds, often called Universal Pre-K (UPK). These programs are usually run through local school districts or licensed providers and are designed to prepare children for kindergarten. Availability can depend on where you live (some areas have a UPK seat for every child, others have limited spots). Learn more in our article What is Universal Pre-K.

-

Head Start: For families who meet income requirements, the federal Head Start program provides free early childhood education (as well as health and nutrition services) for children ages 3–5. Head Start has been a model for expanding access to preschool nationwide. (See our blog post on The Head Start model and making universal preschool a reality for more on this topic.)

-

Free Preschool Programs: Aside from UPK and Head Start, there may be other free or low-cost preschool options in your area. Non-profit organizations, co-op preschools, or state/local scholarships can sometimes help cover preschool tuition. To explore these options and find programs near you, check out our guide on How to find free preschool.

In short, Education Savings Accounts won’t cover costs before kindergarten, but once your child is school-aged, an ESA (if available in your state) can be a valuable resource to customize and fund their K–12 education. For the preschool years, take advantage of publicly-funded Pre-K programs or the resources above to ensure your child is ready to thrive when they do enter Kindergarten.